What SoFi Is Rolling Out & Why It Matters

SoFi Technologies Inc (SOFI)

SoFi Technologies Inc is an equity in the USA market.

The price is 26.38 USD currently with a change of 1.14 USD (0.05%) from the previous close.

The latest open price was 25.74 USD and the intraday volume is 23912182.

The intraday high is 26.6 USD and the intraday low is 25.31 USD.

The latest trade time is Monday, October 6, 10:22:52 EDT.

The new “Options Level 1” launch

On October 2, 2025, SoFi announced that it is expanding its SoFi Invest platform to support “Level 1” options , namely the ability for eligible users to sell covered calls and write cash-secured puts through the SoFi app. (Investopedia) The offering comes with zero commissions, no contract fees, and waived exercise/assignment fees (though regulatory fees may still apply). (Barron's) SoFi also emphasizes built‑in educational content to help users understand risks. (Investopedia)

This new capability builds on SoFi’s existing options services (what the company refers to as “Level 2” strategies, such as buying protective puts) and signals a broader ambition: expand the investing product suite, deepen customer engagement (“stickiness”), and eventually introduce more advanced strategies (e.g. options in IRAs, zero‑days-to-expiration). (Barron's)

SoFi itself formalized the launch via a press release. (SoFi Investors) Their investor blog and support pages also describe how the options feature will operate (approval process, order types, risk disclosures). (SoFi)

Thus, we are not speculating , this is an actual product expansion, not just a rumor.

B. Strategic Rationale: Why SoFi is doing this now

From a business-strategy lens, this move fits SoFi’s vision of being an “all-in-one” financial services hub (banking, lending, investing, payments, etc.). Offering options trading can:

Boost engagement and retention. Users who trade options tend to be more active and vested in their brokerage platform. SoFi can better “lock in” users to its ecosystem (loans, accounts, wallets) by expanding its investable products.

Differentiate and compete. Many established brokers (Charles Schwab, Fidelity, TD Ameritrade, etc.) already offer options trading. To stay competitive, SoFi needs to match or exceed features. The no‑commission / no-fee stance is a competitive lever.

Drive potential incremental revenue (even if modest). Although SoFi waives many fees, there may still be regulatory or clearing-related revenue (or cost offsets), margin lending, interest on collateral, or future premium feature monetization.

Upsell path to more complex offerings. Once users are comfortable with simpler strategies (covered calls, cash-secured puts), SoFi can introduce more advanced options types or leverage as user sophistication evolves.

Data, cross-sell, and “flywheel” effects. More trading activity yields more data, which can inform product design, risk management, and cross-selling (loans, credit cards, banking, etc.).

In fact, analysts and commentators had anticipated this long ago as a logical next step in SoFi’s growth playbook. For example, back in March 2022, The Motley Fool wrote:

“Options trading could be a big deal for SoFi because it makes the Invest product more attractive … brings more members into the SoFi ecosystem … may improve revenue in the company’s Financial Services division.” (The Motley Fool)

Thus, this is a strategically coherent expansion , though it also carries risks (which we’ll examine).

II. Potential Impacts on SoFi the Company & Its Stock

Adding an options platform is not just a product decision , it can influence SoFi’s business metrics, valuation, and market perception. Below are key areas of impact (positive and negative).

A. Revenue / profit dynamics

Fee compression vs. margin sources. On one hand, by waiving commissions and contract fees, SoFi is foregoing a classic revenue stream from options trading. That could strain profitability if volume is low. On the other hand, options-related collateral, margin lending, and interest income could offset part of that forgone revenue. The net is uncertain early on.

Incremental volume and capital flows. If a meaningful segment of users adopt options trades (especially high-propensity traders), SoFi may benefit from increased assets under custody, more cash balances, and ancillary flows (e.g. margin accounts).

Cross-sell boost. Users engaging with invest products might be more likely to also take out loans, credit products, or use SoFi’s deposit/interest accounts, strengthening SoFi’s revenue mix.

Cost / risk and compliance burden. Options trading adds complexity (clearing, risk controls, regulatory oversight). SoFi will need to staff, monitor, and manage the infrastructure, which will raise operating costs.

Latency, pricing, execution quality. Users may quickly evaluate the quality of executions, slippage, and reliability. If SoFi cannibalizes goodwill by underperforming peers, that can damage brand trust.

Thus, in the near term, the impact on SoFi’s bottom line is likely modest or neutral (perhaps slightly negative), but the medium-to-longer term upside is more interesting if the product gains traction.

B. Investor Sentiment & Valuation

Market reaction. Already, the news triggered a ~1% stock gain. (Investopedia) This suggests the market views the move positively (i.e. “this is growth, not a distraction”).

Multiple expansion potential. If SoFi can reliably convert a fraction of its user base into active options traders and monetize that, analysts might assign a higher multiple for its FinTech/investing vertical.

Volatility and risk premium. With more trading activity and derivatives exposure, investors may demand a higher risk premium (i.e. expect more volatility). That could increase implied volatility pricing, option hedging flows, and margins of safety.

Earnings guidance / forward estimates. If SoFi begins disclosing metrics around options product adoption , e.g. options volume growth, impact on user retention , that can anchor future expectations. Upward divergences vs. plan could be rewarded; misses punished.

Competition risk and regulatory sensitivity. The move also raises stakes , if execution is subpar, or regulatory scrutiny tightens (e.g. oversight on retail derivatives), SoFi will feel stronger headwinds. The market will watch metrics like complaint rates, margin blowups, and risk events.

C. Risks & Downside Scenarios

Low adoption. If few users choose to use options trading, SoFi may end up bearing fixed costs without meaningful incremental revenue or retention benefit.

Risk events / trading losses. Retail options trading sometimes leads to outsized losses or flash crashes (especially with zero-day expirations). SoFi must manage clearing risk, risk controls, and defaults. A high-profile event could hurt the brand.

Margin blowups and bad debt. If SoFi extends margin and users default, SoFi may absorb losses (or need strong risk provisioning).

Execution / latency inferiority. If SoFi cannot match execution prices or platform stability of established brokers (TD Ameritrade, Interactive Brokers, etc.), users may prefer to trade elsewhere, undermining the offering.

Regulatory / audit risk. As options trading for retail is closely monitored (e.g. FINRA, SEC), missteps in disclosures, suitability, or margin practices could attract enforcement or fines.

Cannibalization. Some users currently trading through competitor platforms might move to SoFi, but the real benefit depends on whether SoFi captures new volume or displaces competitors , cannibalization alone might offer limited net gains.

D. Longer-Term Strategic Leverage

If SoFi succeeds, the options platform adds another dimension:

It deepens the “financial super app” narrative , not just banking or lending, but a full investing stack.

It allows SoFi to target more engaged / active trader segments, expanding the user base with more “hyperactive” users.

It may open new monetization paths: premium data, advanced analytics, faster execution tiers, margin tiers, or even sell-side (market-making, order-flow) relationships.

It could feed into AI / quantification strategies, leveraging aggregated options behavior data (e.g. implied volatility skew, flow signals) to design new products or insights.

Thus, while cautious in the near term, the strategic upside is meaningful if adoption scales.

III. Impact on the Broader Options Market

SoFi entering more actively into retail options may influence the broader U.S. options ecosystem in several interesting ways.

A. Increased Retail Flow & Liquidity

As SoFi brings in additional retail participants (especially new or semi-active ones), the aggregate order flow in equity options might increase modestly. This can:

Raise liquidity in less-traded underlyings (especially smaller names)

Add competition for execution venues (spotting bottlenecks or congestions)

Increase competitive pressure on fees (already low, but pushing brokers to maintain or cut)

The more retail options participants, the more robust the market depth and pricing efficiency (particularly around strikes with less activity).

B. Price Discovery & Volatility Signals

More retail flow (especially in directionally biased strategies) may amplify gamma / vega feedback loops (especially at short-dated expirations). In volatile names, this may increase intraday swings or gamma squeezes , particularly if many users adopt zero-day or short-duration plays in the future.

As SoFi adds more users, the retail options order flow may become a more noticeable input to institutional hedging and volatility pricing , similar to how “flow-based” market signals (like options skew, delta hedges) are used increasingly in quant strategies.

C. Fee and Business Pressure on Brokers / Market Makers

With SoFi offering zero commissions and no contract fees, competitors may feel continued pressure to maintain or improve their cost structures (rebates, spreads, clearing yields). This could drive further commoditization in the options‑execution space, pushing margins down for brokers and market makers.

Also, the clearing, routing, and custodian infrastructures will see more demand; firms may need to scale systems and manage more retail options volume.

D. Risk Management & Systemic Sensitivities

More leverage and retail options activity across brokers increases systemic sensitivity to large market moves. If many retail users are over-levered or at risk during volatility surges, brokers (including SoFi) must manage tail exposures carefully. A widely adopted product like SoFi’s can become part of “tail risk plumbing” in derivatives markets.

Regulators may also monitor retail options usage more scrutinously if adverse events (e.g. mass defaults, failed margin calls) spike.

Hence, SoFi’s entrance is incremental but adds to cumulative pressures in options market infrastructure, oversight, and behavior.

IV. SoFi (SOFI) as an Options-Traded Underlying: What Changes?

When a company like SoFi expands its own options platform, it changes dynamics around how the market treats the stock in its derivatives markets. Below, I break down how SoFi’s own underlying might see unique shifts.

A. Increased option interest in SOFI

By enabling easier options activity for SoFi users, more investors might trade options on SOFI itself. Already, the options chain on SOFI is active: according to GuruFocus, about 275,000 contracts are traded with a put/call ratio of ~0.64 and implied volatility (IV30) elevated (~66%). (GuruFocus) Recent unusual activity in SOFI options suggests traders are targeting wide ranges (e.g. $3–$40) in expectation of large moves. (Nasdaq)

Additionally, SOFI began offering new January 2025 options contracts in late 2024. (Nasdaq) And in some option-strategy guides, analysts have suggested cash-secured puts or covered calls on SOFI yield ~6% returns (in favorable scenarios) due to its high implied volatility. (Investors.com)

Thus, the option market already has decent interest in SOFI; the new product expansion may amplify that.

B. Implied Volatility, Skew, and Pricing Effects

With more trading in SOFI’s options:

Higher implied volatility may become more persistent, because increased demand for hedging or speculative trades pushes option prices higher.

Skew asymmetry (put vs call) may evolve, perhaps steepening if more downside protection is sought.

Liquidity and tighter spreads. With more volume, bid-ask spreads may compress, making trading SOFI options more appealing for retail and professional traders.

Gamma / vega exposure. Market makers will need to adjust hedging more actively, potentially leading to feedback loops , especially around earnings, news, or volatility shocks.

C. Correlation With Stock Moves & Feedback Loops

Because SoFi is the entity enabling the options trades, stock moves (especially upward or during news) might attract more retail options flow, which in turn may amplify further moves (positive feedback). For instance, if SOFI stock begins rallying, users may buy calls (pushing further demand), which forces market makers to buy underlying stock (delta hedging). That can accelerate moves , especially in a smaller-cap or midcap equity like SOFI.

Conversely, downward pressure or volatility might lead to more protective puts being purchased, increasing hedging flows , again feeding price action. Thus the options activity could be more self-referential.

D. Risk of Overhang & Imbalances

If many retail traders write covered calls or sell cash-secured puts, there may be a supply of short option open interest that, in extreme market moves, gets forced to adjust (exercise, assignment). This can create overhangs or distortions if many participants are in the same direction. SoFi must monitor default risk, assignment logistics, and liquidity to manage such extremes.

V. Market Data & Sentiment Check

Here is a snapshot of current market dynamics around SoFi and its options:

Stock price: $26.38 as of latest trading.

Options activity: Moderate but growing interest; put/call ratio ~0.64 (i.e. more calls than puts) per GuruFocus analysis. (GuruFocus)

Implied volatility: Elevated , in some reports, ~66% for 30-day implied volatility. (GuruFocus)

Unusual flow: Some option flow aggregators flag wide-range expectations (e.g. $3–$40). (Nasdaq)

Stock momentum: Recently, SoFi stock had a strong move earlier in 2025: it surged ~19% after Q2 results and raised guidance. (The Wall Street Journal)

Analyst consensus: Some upward estimate revisions; consensus estimates for earnings in past months have tilted more positive. (Nasdaq)

On the social / retail side:

In Reddit threads, users longtime demanded options capability; when SoFi first rolled out options (in 2022), the reception was enthusiastic but cautious:

“After countless requests, options trading is finally available … we’re launching an options trading platform that’s user‑friendly …” (Reddit)

But also warnings:

“Once flagged as a daytrader, YOU CANNOT EXIT POSITION so your order will be forced to be expired … be careful guys.” (Reddit)

“We still offer options trading! If you’re having issues, contact support.” (Reddit)These reflect early user pains (bugs, restrictions) that SoFi must iron out if the product is to scale.

In SoFi’s own channels, they have published support documentation on order types, approval, and risk disclosures. (SoFi) Also their press release frames the new offering as “helping members pursue risk-adjusted strategies” with education baked in. (SoFi Investors)

Thus overall, sentiment is cautiously optimistic , the market sees promise, but is watching execution.

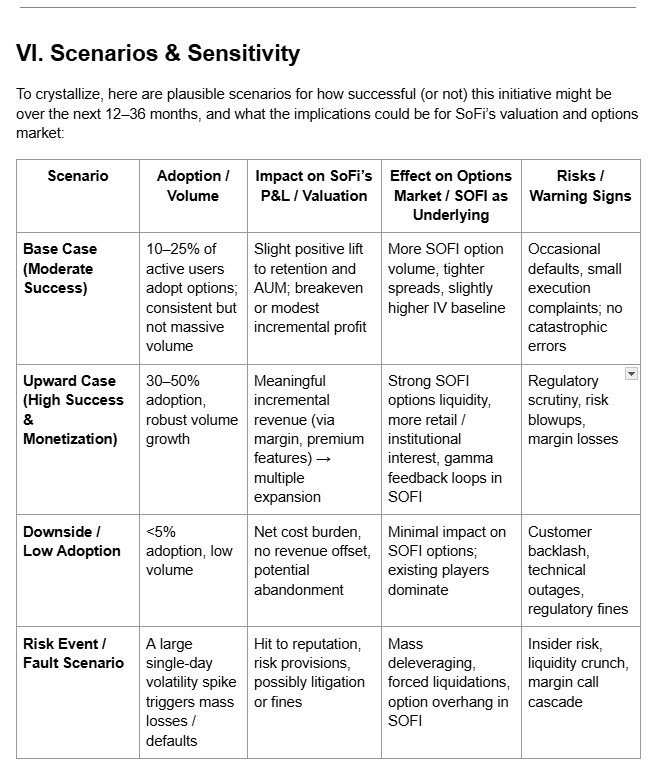

The valuation sensitivity is worth highlighting: SoFi’s stock is now partly priced for growth momentum. If the options product becomes a recognized contributor to user retention and revenue, then forward multiples could expand by 10–30% relative to peers. However, a stumbles or risk event could lead to multiple contraction.

VII. Recommendations & What to Watch

If you’re an investor, here are key metrics and signs to monitor as SoFi’s options platform evolves:

Adoption metrics , how many users are approved for options, how many actively use it, and the volume per user.

Revenue / margin contribution , interest, margin spread, subscription or premium features, net of costs.

Execution quality metrics , slippage, fill rates, latency compared to major brokers.

Risk event tracking , default rates on margin, forced liquidations, regulatory complaints.

Options flow and open interest in SOFI , changes in volume, skew, and implied volatility over time.

Competitive responses , what other brokers do in response; whether they cut fees or introduce bold features.

Regulatory / legal oversight , any warnings or actions from SEC, FINRA, CFPB regarding retail options practices.

From a strategic angle, SoFi should prioritize:

Ensuring the platform is stable, reliable, and execution is competitive.

Phasing advanced strategies gradually so risk is controlled.

Transparent communication around risk, metrics, and limitations.

Leveraging options behavior data to inform product design and cross-sell.

Conclusion

SoFi’s move to launch Options Level 1 capabilities is a material step in its evolution from fintech/lending platform toward a full-stack financial super app. The potential upside is meaningful: deeper engagement, new revenue levers, improved competitiveness, and derivative-market relevance. At the same time, risks abound , from adoption uncertainty, cost burdens, execution pitfalls, to regulatory scrutiny.

For its stock (SOFI), this expansion may contribute to multiple expansion and investor confidence , but the real test lies in execution and adoption. For the broader options market, additional retail flow, competitive pressures, and feedback loops could become more pronounced. And for SOFI as an underlying, the ramp in option volume, skew dynamics, and gamma-driven feedback could reshape how trading in its derivatives behaves.

Ultimately, this is a bold, logical extension of SoFi’s vision, and whether it becomes a “home run” or a cautionary tale will hinge on execution, risk management, and user uptake.

5 FAQs

Q1. Why did SoFi choose to start with Level 1 strategies (covered calls / cash-secured puts) rather than full options types?

Because Level 1 strategies are relatively lower risk, simpler to understand, and easier to monitor for compliance and risk controls. For a first rollout, limiting to these helps SoFi scale responsibly, build familiarity, and manage default risks before enabling more advanced strategies.

Q2. Will SoFi make money from options if it’s waiving commissions and contract fees?

Possibly, though not massively initially. SoFi may earn via margins on collateral, interest on cash balances, premium “upgrade” features, or offset via cross-sell. But in early stages, volume and adoption will matter more than pure fee income.

Q3. Could options activity amplify volatility in SoFi’s stock?

Yes. If many retail users trade calls or puts on SOFI, market makers must hedge dynamically (delta hedging), potentially pushing stock moves further in one direction (gamma feedback). This is particularly true around news, earnings, or abrupt volatility.

Q4. What risks does SoFi face from regulatory oversight or compliance?

Retail options trading is under scrutiny by agencies like SEC, FINRA, and CFPB. Issues like suitability, margin practices, disclosures, defaults, system outages, or customer complaints could attract fines or enforcement if not handled prudently.

Q5. Does SoFi’s new options platform guarantee success?

No. Success depends heavily on user adoption, volume, execution quality, risk management, and competitive differentiation. While the strategic rationale is sound, the challenges are substantial. Execution will be everything.